Why most banks charge customers interest rates to borrow money?

Because a company that lends money (e.g., bank) does not have access to the money that is lent and needs to make a profit, borrowers must pay a fee, called interest, to receive a loan.

Interest is charged on loans to cover the cost of obtaining funds and the cost incurred in the process of borrowing and lending.

A bank's main source of income is the revenue it earns from the interest a bank receives on the money it lends to its customers. To put it very simply, banks earn money by charging more interest on loans than that they pay on savings. In banking language this is referred to as the net interest spread.

So they pay interest to entice you to keep your money in your savings account. “You're essentially loaning money to the bank, and the bank is paying you an interest rate for that loan,” says Anderson Lafontant, a certified financial planner with Miracle Mile Advisors.

The prime rate is the current interest rate that financial institutions in the U.S. charge their best customers.

Unsurprisingly, bond buyers, lenders, and savers all benefit from higher rates in the early days. Bond yields, in particular, typically move higher even before the Fed raises rates, and bond investors can earn more without taking on additional default risk since the economy is still going strong.

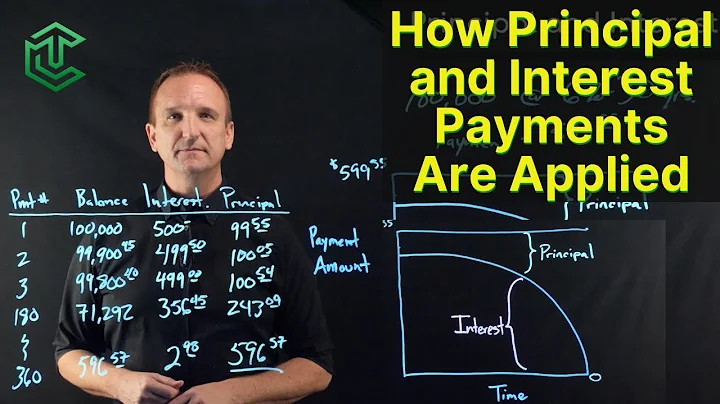

The primary source of income for banks is the difference between the interest charged from the borrowers and the interest paid to the depositors. Banks usually collect higher interest from loans than the interest they provide for deposits.

Solution: Banks charge higher interest on loans than what they offer on deposits. Banks take deposits from the public and give interest on these deposits. Banks, after all, are also profit-making organizations; thus, most of the deposits are used to lend to borrowers.

You can look to see the amount of total deposits that a bank has and look to see whether they have been increasing over time. A strong track record of stable growth is an indicator of consumer confidence and the bank's ability to strengthen its balance sheet.

Both certificates of deposit (CDs) and share certificates are low-risk deposit accounts where your money can grow at a fixed rate. The main distinction between them is that CDs are products offered by for-profit banks, while share certificates are offered by member-owned, not-for-profit credit unions.

Which savings account will earn you the least money?

Traditional savings accounts are the most common. They offer a secure place to store your money, but the interest rates are often lower compared to other options. High-yield savings accounts, on the other hand, provide higher interest rates, allowing your money to work harder for you.

Savings, money market, CD and rewards checking accounts are among the safest places for your money, as long as your bank or credit union is insured by the Federal Deposit Insurance Corp. or the National Credit Union Administration.

Currently, no banks are offering 7% interest on savings accounts, but some do offer a 7% APY on other products. For example, OnPath Federal Credit Union currently offers a 7% APY on average daily checking account balances up to and under $10,000.

- EverBank Performance℠ Savings: 5.15% APY.

- Bask Interest Savings Account: 5.10% APY.

- LendingClub High-Yield Savings Account: 5.00% APY.

- Varo Savings Account: 3.00% to 5.00% APY.

- Laurel Road High Yield Savings®: 5.00% APY.

- Quontic Bank High Yield Savings: 4.50% APY.

When interest rates are higher, banks make more money by taking advantage of the greater spread between the interest they pay to their customers and the profits they earn by investing. A bank can earn a full percentage point more than it pays in interest simply by lending out the money at short-term interest rates.

The Fed has two ways of influencing the economy. It can impact interest rates by moving an interest rate it directly controls. The Fed also has the power to change the supply of money in the economy.

Higher interest rates typically slow down the economy since it costs more for consumers and businesses to borrow money. But while higher interest rates can make it more expensive to borrow and could hamper overall economic growth, there are also some benefits.

Banks can borrow at the discount rate from the Federal Reserve to meet reserve requirements. The Fed charges banks the discount rate, commonly higher than the rate that banks charge each other.

Debt can be used as leverage to multiply the returns of an investment but also means that losses could be higher. Margin investing allows for borrowing stock for a value above what an investor has money for with the hopes of stock appreciation.

The Primary Way That Banks Make Their Money. The main way that banks make money is from their customers who deposit with them. They then use that money to then lend to other customers.

What is the safest place for keeping money?

In conclusion, a bank is considered the safest place for keeping money due to its stringent security measures, insurance coverage, legal protection, accessibility, convenience, and professional management.

Any individual can open savings bank accounts singly or jointly. A joint account is one, which operated by two or more persons. SB accounts of minors can be opened jointly with a natural guardian/legal guardian.

Banks are generally free to determine the interest rate they will pay for deposits and charge for loans, but they must take the competition into account, as well as the market levels for numerous interest rates and Fed policies.

| Bank | Forbes Advisor Rating | Learn More |

|---|---|---|

| Chase Bank | 5.0 | Learn More Read Our Full Review |

| Bank of America | 4.2 | |

| Wells Fargo Bank | 4.0 | Learn More Read Our Full Review |

| Citi® | 4.0 |

Wells Fargo (WFC)

Nevertheless, it finds itself as one of the least likely financial institutions to fail. Interestingly, since the Jan. opener, WFC gave up more than 13% of equity value.

References

- https://www.kiplinger.com/personal-finance/banking/citi-plans-to-put-you-into-relationship-tiers-next-year

- https://www.chime.com/bank-fees/citibank-banking-fees/

- https://homework.study.com/explanation/what-are-the-primary-reasons-that-lenders-charge-interest-on-loans.html

- https://www.fdic.gov/consumers/consumer/moneysmart/podcast/documents/checking-accounts-checking-account-fees.pdf

- https://cals.ncsu.edu/news/you-decide-is-the-fed-done-raising-interest-rates/

- https://www.nerdwallet.com/article/credit-cards/what-is-a-good-apr-for-a-credit-card

- https://www.cbsnews.com/news/why-you-should-deposit-10000-into-a-high-yield-savings-account-now/

- https://www.bankrate.com/banking/avoid-bank-fees-and-penalties/

- https://www.pwc.com/ug/en/press-room/capping-interest-rates.html

- https://online.citi.com/US/ag/worldwide-atm-network

- https://www.esl.org/resources-tools/educational-resources/understanding-the-prime-rate

- https://www.aussie.com.au/insights/articles/how-can-i-negotiate-with-my-lender-to-get-a-better-rate/

- https://www.investopedia.com/terms/b/bank-fees.asp

- https://time.com/personal-finance/article/how-is-credit-card-interest-calculated/

- https://www.toppr.com/ask/question/distinguish-betweenbank-rate-and-rate-of-interest/

- https://www.investopedia.com/financial-edge/0710/5-ways-debt-can-make-you-money.aspx

- https://portal.ct.gov/DOB/Consumer/Consumer-Education/ABCs-of-Banking---Banks-and-Our-Economy

- https://www.financestrategists.com/banking/interest-rate/

- https://www.nerdwallet.com/article/banking/what-the-fed-rate-increase-means-for-savings-accounts

- https://www.schwab.com/learn/story/potential-winners-and-losers-higher-interest-rates

- https://www.equifax.com/personal/education/credit/score/articles/-/learn/what-is-a-good-credit-score/

- https://www.linkedin.com/pulse/how-negotiate-lower-interest-rate-your-loan-rohit-kumar-mahto

- https://www.rba.gov.au/education/resources/explainers/banks-funding-costs-and-lending-rates.html

- https://www.citi.com/banking/simplifiedbanking

- https://www.chase.com/personal/credit-cards/education/interest-apr/when-does-interest-start-to-accrue-on-credit-card

- https://www.cnet.com/personal-finance/banking/savings/these-high-yield-savings-accounts-earn-5-percent-apy-or-more/

- https://fortune.com/recommends/banking/best-savings-accounts/

- https://www.linkedin.com/pulse/why-banks-need-focus-over-gen-z-banking-habits-viliana-petrova

- https://www.bankrate.com/banking/reviews/capital-one/

- https://www.marketwatch.com/guides/banking/citibank-review/

- https://byjus.com/question-answer/identify-the-main-source-of-income-for-banks/

- https://mozo.com.au/savings-accounts/articles/how-to-triple-the-interest-on-your-savings-today

- https://themortgagereports.com/18709/mortgage-rate-negotiation-lending-gina-pogol

- https://www.nerdwallet.com/article/loans/personal-loans/usury-laws

- https://www.cnbc.com/select/negotiating-mortgage-rates/

- https://www.findlaw.com/state/california-law/california-interest-rates-laws.html

- https://www.bankrate.com/banking/does-closing-bank-accounts-hurt-credit/

- https://www.usnews.com/banking/reviews/citibank

- https://www.bankrate.com/banking/cds/cd-vs-share-certificate/

- https://www.credit.org/blogs/blog-posts/what-are-interest-rates-how-does-interest-work

- https://wallethub.com/answers/cc/what-is-24-apr-on-a-credit-card-1000248-2140743241/

- https://www.sofi.com/learn/content/can-you-negotiate-a-higher-savings-rate/

- https://www.bankrate.com/finance/credit-cards/good-apr-for-credit-card/

- https://money.com/capital-one-360-performance-savings-high-yield-savings-accounts-review/

- https://www.fitchratings.com/research/banks/fitch-affirms-capital-one-at-a-f1-outlook-stable-21-02-2024

- https://www.forbes.com/advisor/banking/savings/capital-one-savings-account-rates/

- https://homework.study.com/explanation/it-is-possible-for-an-advising-bank-negotiating-bank-and-confirming-bank-to-be-the-same-bank-in-a-particular-letter-of-credit-explain.html

- https://www.bankrate.com/finance/credit-cards/does-law-cap-credit-card-interest-rates/

- https://www.citibank.com.sg/pdf/0323/citibank-pricing-guide.pdf

- https://finance.yahoo.com/news/7-bank-stocks-least-likely-192442317.html

- https://www.forbes.com/advisor/banking/safest-banks-in-the-us/

- https://www.capitalone.com/bank/savings-accounts/online-performance-savings-account/

- https://fortune.com/recommends/credit-cards/whats-is-a-good-apr-for-a-credit-card/

- https://www.investopedia.com/insights/forces-behind-interest-rates/

- https://fortune.com/recommends/banking/how-interest-works-on-savings-account/

- https://www.fool.com/the-ascent/banks/why-interest-rates-low-savings/

- https://www.smartaboutmoney.co.za/debt/working-with-credit/who-sets-the-interest-rates-and-how-do-they-affect-me/

- https://www.moneycontrol.com/news/business/personal-finance/want-a-lower-interest-rate-on-your-home-loan-heres-how-you-can-get-it-11908861.html

- https://www.creditninja.com/blog/where-do-banks-get-money-to-lend-to-borrowers/

- https://www.visiolending.com/blog/how-are-commercial-loan-rates-determined

- https://www.coursesidekick.com/economics/244055

- https://www.moneysupermarket.com/savings/saving-lump-sum/

- https://www.businessinsider.com/personal-finance/what-is-the-prime-rate

- https://www.cnbc.com/select/how-to-avoid-bank-fees/

- https://www.lendingtree.com/personal/how-to-refinance-a-personal-loan/

- https://wallethub.com/answers/pl/is-a-5-apr-good-1000431-2140750773/

- https://www.investopedia.com/will-2024-mortgage-rates-fall-clues-from-wednesdays-fed-announcement-8611482

- https://www.53.com/content/fifth-third/en/financial-insights/personal/financial-education/pros-cons-of-rising-interest-rates.html

- https://www.cnbc.com/select/how-to-avoid-common-checking-account-fees/

- https://www.cnbc.com/select/how-to-lower-credit-card-interest-rate/

- https://fortune.com/recommends/banking/how-much-money-should-you-keep-in-savings/

- https://www.investopedia.com/terms/p/primerate.asp

- https://www.cnbc.com/select/interest-rates-rising-saving-more-appealing-debt-more-harmful/

- https://www.rocketmortgage.com/learn/how-are-mortgage-rates-determined

- https://www.investopedia.com/articles/investing/080713/how-banks-set-interest-rates-your-loans.asp

- https://www.lendingtree.com/home/mortgage/negotiate-with-mortgage-lender/

- https://www.cnet.com/personal-finance/banking/advice/ways-to-save-money-and-earn-interest/

- https://www.mx.com/blog/how-banks-generate-income-revenue/

- https://www.latimes.com/compare-deals/credit-cards/guides/good-apr-for-credit-card

- https://www.forbes.com/advisor/banking/checking/best-no-fee-checking-accounts/

- https://www.businessinsider.com/personal-finance/5-percent-interest-savings-accounts

- https://www.citibank.com.ph/personal-banking/deposits/savings-account/online-savings-account/

- https://www.clearviewfcu.org/Resources/Learn/Blog/What-Is-the-Prime-Rate-and-Why-Does-It-Matter

- https://www.usnews.com/banking/articles/do-you-pay-taxes-on-savings-account-interest

- https://www.capitalone.com/bank/fdic/

- https://www.investopedia.com/articles/investing/052814/these-sectors-benefit-rising-interest-rates.asp

- https://www.consumerfinance.gov/ask-cfpb/what-is-the-difference-between-a-loan-interest-rate-and-the-apr-en-733/

- https://www.forbes.com/advisor/credit-cards/what-is-a-good-apr-for-a-credit-card/

- https://www.fool.com/the-ascent/banks/savings-accounts/capital-one-360-performance-savings-review/

- https://www.online.citibank.co.in/nrvfaq.htm

- https://www.icicibank.com/blogs/home-loan/how-to-reduce-home-loan-rate

- https://www.forbes.com/advisor/banking/savings/best-high-yield-savings-accounts/

- https://www.bankrate.com/finance/credit-cards/what-to-do-after-card-apr-increase/

- https://www.usnews.com/banking/articles/benefits-of-having-a-savings-account

- https://www.linkedin.com/advice/0/how-can-you-prepare-convincing-case-show

- https://www.investopedia.com/ask/answers/072815/why-do-commercial-banks-borrow-federal-reserve.asp

- https://www.lendingtree.com/credit-cards/articles/apr-ranges-explained/

- https://www.experian.com/blogs/ask-experian/what-factors-do-lenders-consider-when-determining-my-interest-rate/

- https://www.lendingtree.com/home/refinance/lower-mortgage-rate-without-refinancing/

- https://www.depositaccounts.com/banks/health.aspx

- https://www.bankrate.com/finance/credit-cards/citi/

- https://corporatefinanceinstitute.com/resources/commercial-lending/types-of-interest/

- https://www.investopedia.com/terms/c/commercialbank.asp

- https://www.rocketmoney.com/learn/personal-finance/prime-rate

- https://www.nerdwallet.com/article/credit-cards/credit-card-interest-rates-high

- https://www.investopedia.com/terms/f/federal_discount_rate.asp

- https://www.citi.com/banking/checking-account

- https://www.latimes.com/compare-deals/banking/savings/7-percent-interest-savings-accounts

- https://www.capitalone.com/bank/disclosures/online-banking/faqs/

- https://www.equifax.com/personal/education/debt-management/articles/-/learn/debt-negotiation-with-lenders/

- https://edurev.in/question/3530788/The-safest-place-for-keeping-money-a-A-pit-dug-in-the-groundb-An-iron-boxc-Bankd-Money-lenderCorrect

- https://fortune.com/recommends/banking/common-bank-fees-and-how-to-avoid-them/

- https://www.citi.com/banking/personal-banking-guide/basic-finance/how-to-open-a-checking-account

- https://wallethub.com/answers/cc/citibank-annual-fee-1000318-2140753337/

- https://smartasset.com/credit-cards/what-is-a-good-apr

- https://infinitylearn.com/surge/question/economics/banks-charge-higher-interest-rates-on-loans-than-what-they-o/

- https://byjus.com/question-answer/what-is-the-rate-of-interest-at-which-commercial-banks-borrow-money-from-the-rbi/

- https://www.bankrate.com/banking/checking/how-to-avoid-monthly-fees/

- https://blog.seedly.sg/waive-credit-card-annual-fees-singapore-guide/

- https://www.bench.co/blog/tax-tips/small-business-tax-deductions

- https://bankofmaharashtra.in/savings-account

- https://www.citi.com/banking/enhanced-direct-deposit

- https://www.moneysavingexpert.com/savings/best-regular-savings-accounts/

- https://www.newsweek.com/vault/banking/savings/7-percent-savings-account-interest-rates/

- https://www.investopedia.com/ask/answers/041015/how-do-interest-rate-changes-affect-profitability-banking-sector.asp

- https://www.experian.com/blogs/ask-experian/how-to-avoid-bank-fees/

- https://www.usnews.com/banking/articles/how-many-savings-accounts-should-you-have

- https://lottie.org/fees-funding/best-savings-accounts-for-over-60s/

- https://www.citibank.com.sg/personal-banking/deposits/savings-account/basic-bank-account/

- https://www.indiabullshomeloans.com/blog/reduce-your-interest-rate-with-these-3-simple-steps

- https://www.capitalone.com/bank/disclosures/savings-accounts/online-savings-account/

- https://www.linkedin.com/pulse/which-savings-account-earn-you-least-money-sunil-varma-ebjpf

- https://www.investopedia.com/capital-one-savings-account-interest-rates-7497281

- https://www.imf.org/en/Publications/fandd/issues/Series/Back-to-Basics/Banks

- https://www.citi.com/banking/personal-banking-guide/basic-finance/how-to-withdraw-money-from-bank

- https://www.minneapolisfed.org/article/2000/how-do-lenders-set-interest-rates-on-loans

- https://www.moneysavingexpert.com/savings/savings-accounts-best-interest/